The True Cost of DIY Accounting: Hidden Risks and Missed Opportunities

You started your business because you're good at what you do. Maybe you're a consultant, a contractor, a creative, or a service provider. Somewhere along the way, you decided to handle your own books. It made sense at the time: why pay someone else when you can do it yourself?

Here's the thing: that decision might be costing you more than you realize. And we're not just talking about dollars. We're talking about time, peace of mind, missed opportunities, and risks that quietly compound in the background while you're focused on running your business.

Let's break down what DIY accounting actually costs: and help you decide if it's really worth it.

The "Free" Myth: Your Time Has Value

The most common reason business owners handle their own accounting is simple: it feels free. No monthly invoice from a bookkeeper. No advisory fees. Just you, a spreadsheet (or maybe QuickBooks), and a few hours here and there.

But let's do the math.

If you spend even five hours a month on bookkeeping, reconciling accounts, categorizing transactions, and prepping for taxes, that's 60 hours a year. Now ask yourself: what's your hourly rate? What could you bill clients during that time? What strategic work could you be doing instead?

Hours spent on data entry are hours not spent on revenue-generating activities. That's not just a missed opportunity: it's a real cost. Research shows that this time diversion leads to missed business opportunities and a lack of strategic direction. You're essentially paying yourself to do work that someone else could handle more efficiently.

And here's the kicker: most business owners underestimate how much time they actually spend on financial tasks. It's not just the monthly reconciliation. It's the scramble before quarterly estimates. The panic when you can't find a receipt. The Sunday night spent catching up because you fell behind.

That time adds up faster than you think.

Missed Deductions: Money Left on the Table

Here's where DIY accounting gets expensive in a very tangible way.

When you're not a tax professional, you don't know what you don't know. You might be categorizing expenses correctly enough to pass a basic sniff test, but are you maximizing your deductions? Are you aware of every credit you qualify for? Are you structuring your expenses in a way that minimizes your tax burden legally and strategically?

Studies show that businesses make errors in approximately 40% of their financial records. A single miscategorized transaction can cost hundreds: or even thousands: in unnecessary tax payments. That vendor dinner you wrote off as "meals" instead of "business development"? That home office deduction you skipped because you weren't sure you qualified? That equipment purchase you expensed all at once instead of depreciating strategically?

These aren't hypotheticals. They're real money that business owners leave on the table every single year because they're doing their own books without the expertise to optimize them.

Common missed deductions include:

- Home office expenses (many business owners skip this out of fear)

- Vehicle and mileage deductions (improperly tracked or underreported)

- Professional development and education costs

- Health insurance premiums (especially for S Corp owners)

- Retirement contributions (and the tax strategies around them)

- Software, subscriptions, and tools (often lumped into generic categories)

A professional doesn't just record your transactions: they look for opportunities. That's a fundamentally different approach than simply "keeping the books."

Audit Risk: The Compliance Factor

Nobody wants to hear from the IRS. But if your records are inconsistent, incomplete, or just messy, you're increasing the odds of that dreaded envelope showing up.

The IRS reports that businesses with inconsistent or incomplete records face audit rates three times higher than those with professional bookkeeping. That's not a small difference. That's a significant increase in risk that you're taking on every time you cut corners or "figure it out later."

And audits aren't just stressful: they're expensive. Even if you've done nothing wrong, the time and cost of responding to an audit can be substantial. If errors are found, you're looking at penalties averaging $845 annually, plus interest on unpaid amounts, plus the potential for legal complications that require professional intervention.

Beyond federal taxes, there are state compliance requirements, payroll regulations (if you have employees or pay yourself through payroll), and industry-specific rules that change regularly. DIY bookkeepers frequently fall behind on regulatory updates, creating serious legal and financial risks: including damaged business credit that can affect your ability to secure financing down the road.

Staying compliant isn't just about avoiding penalties. It's about protecting your business's future.

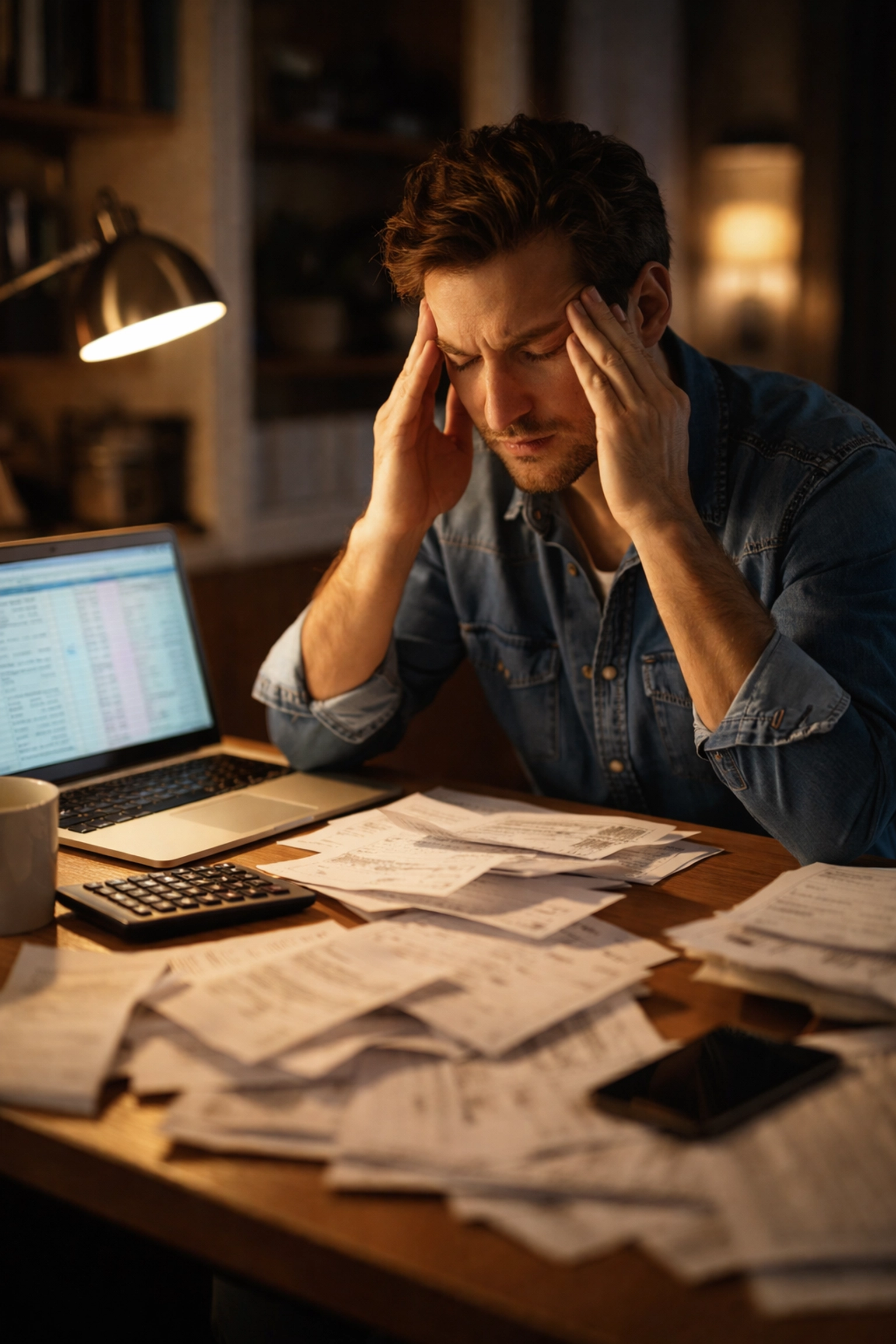

The Mental Toll: Stress You Didn't Budget For

Let's talk about something that doesn't show up on a balance sheet: the mental burden of managing your own finances.

There's a particular kind of stress that comes with financial uncertainty. When you're not confident in your numbers, every business decision feels riskier. Should you hire that contractor? Can you afford that equipment upgrade? Is your pricing actually profitable, or are you just guessing?

Inaccurate financial data prevents informed decision-making. Business owners may believe they're profitable when actually operating at a loss: or vice versa: leading to poor strategic choices. That uncertainty creates a low-grade anxiety that follows you around, even when you're not actively working on your books.

And then there's the deadline panic. Tax season arrives, and suddenly you're scrambling to find documentation, reconcile months of neglected transactions, and figure out why your numbers don't match your bank statements. That panic isn't just unpleasant: it leads to rushed decisions and errors that can have lasting consequences.

The average time to detect and contain a financial error or data issue is approximately 277 days. That's nine months of operating with bad information before you even realize something's wrong.

When DIY Makes Sense (And When It Doesn't)

Look, we're not saying every business owner needs to outsource their accounting immediately. If you're just starting out, have very simple finances, and genuinely enjoy the process, handling your own books can work: for a while.

But there's a tipping point. And most business owners hit it sooner than they expect.

Signs you've outgrown DIY accounting:

- You're consistently behind on reconciling your accounts

- Tax time feels chaotic and stressful

- You're not confident in your profit margins or cash flow

- You've missed estimated tax payments or filed late

- You're making business decisions based on gut feelings rather than data

- You've grown to include employees, contractors, or multiple revenue streams

The goal isn't to make you feel bad about doing your own books. The goal is to help you recognize when the cost of continuing to do it yourself exceeds the cost of getting help.

What Professional Support Actually Looks Like

When you work with an accounting professional, you're not just paying someone to categorize transactions. You're gaining a partner who:

- Catches errors before they become problems

- Identifies deductions and strategies you'd never think of

- Keeps you compliant with changing regulations

- Provides accurate financial reports you can actually use

- Frees up your time for work that moves your business forward

The return on that investment often pays for itself multiple times over: in tax savings, avoided penalties, and reclaimed hours.

The Bottom Line

DIY accounting feels like a money-saving move. But when you factor in the time cost, the missed deductions, the compliance risks, and the mental burden, the math often doesn't add up.

Your expertise is running your business. Ours is making sure the financial side supports your goals instead of holding you back.

If you've been wondering whether it's time to hand off the books, let's talk. A quick conversation can help you understand what professional support would look like for your specific situation: and whether the investment makes sense for where you are right now.

You didn't start your business to become an accountant. Let's make sure your finances reflect that.

Let’s find your way to tax and accounting peace of mind

Let us be part of your journey towards success.